By Kulpreet Singh | Kashbulls Insights

When you are looking for the ultimate “Safety First” investment in India, two names always dominate the conversation: the National Savings Certificate (NSC) and the RBI Floating Rate Savings Bonds (FRSB).

Both are backed by the Government of India, meaning your capital is as safe as it gets. But over the last 15 years, the “winner” between the two has shifted. Here is how to decide which one deserves a spot in your portfolio today.

The 15-Year Evolution: From Fixed to “Shadow”

Historically, these two instruments operated in different worlds.

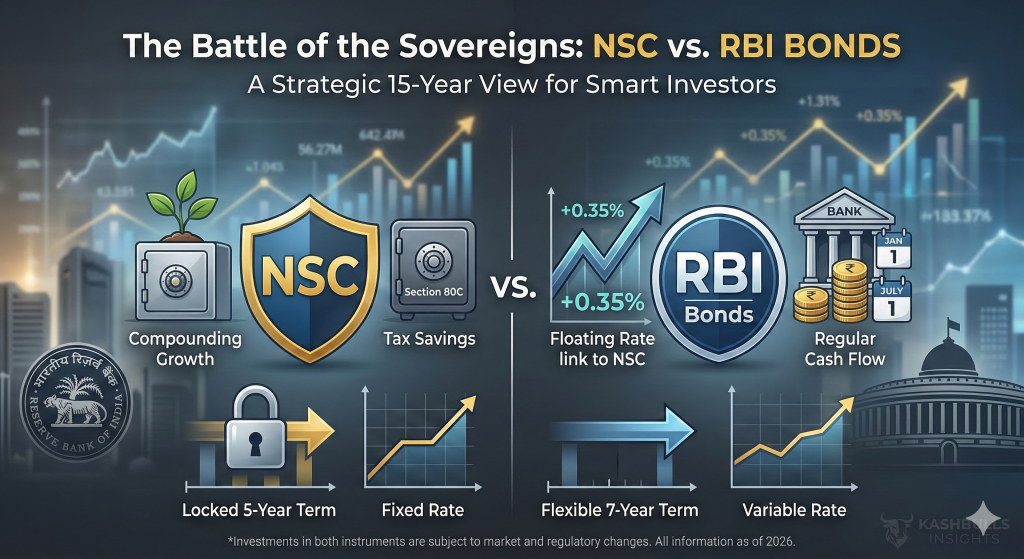

- The Old Guard (2011-2019): Both had fixed rates. You locked in a rate, and that was your reality for 5 to 7 years.

- The New Era (2020-2026): In July 2020, the RBI changed the game. They linked the RBI Bond rate directly to the NSC.

- The Secret Formula: Currently, RBI Bond Rate = NSC Rate + 0.35%. This means the RBI Bond is effectively the “big brother” that always stays exactly 35 basis points ahead of the NSC.

The “Quick-Scan” Comparison

Instead of a standard table, let’s look at the DNA of these two investments:

| The Feature | NSC (The Tax-Saver) | RBI Bond (The Income-Generator) |

| Your Goal | Tax Deduction (80C) + Compounding | High Regular Cash Flow |

| The Interest | Locked: Changes only for new buyers | Fluid: Resets for everyone every 6 months |

| Payout Style | “See you in 5 years” (Cumulative) | “Check your bank” (Every Jan & July) |

| Tax Status | Tax-deductible up to ₹1.5 Lakh | Fully taxable at your slab |

| Loan Value | Banks love it as collateral | Zero (Cannot be pledged for loans) |

Which One Should You Pick? (The Kashbulls Strategy)

Case A: You are in the Accumulation Phase

If you are still building your corpus and haven’t exhausted your ₹1.5 Lakh limit under Section 80C, NSC is the undisputed king. * Why? The interest you earn in the first 4 years is considered “reinvested” and qualifies for a fresh tax deduction each year. It’s a double-win for your tax planning.

Case B: You Need Regular Income

If you are a retiree or looking for a steady quarterly/half-yearly “salary” from your investments, RBI Floating Rate Bonds are superior.

- Why? At 8.05% (current rate), it beats almost all 5-year and 10-year Bank FDs while offering 100% sovereign safety.

Case C: The Interest Rate Gamble

- Choose NSC if you think interest rates in India will fall in the next 12 months. You lock in 7.7% today for 5 years.

- Choose RBI Bonds if you think rates will rise. Since it’s a “floating” bond, your returns will automatically climb higher if the government hikes rates.

4. The Final Verdict

There is no “better” investment—only the “right” investment for your specific goal.

- NSC is a shield (protects your tax and locks in your rate).

- RBI Bonds are an engine (drives regular cash flow with a premium spread).

Confused about where your surplus should go this quarter? At Kashbulls, we don’t just look at rates; we look at your tax slab, liquidity needs, and long-term goals.

[Click here to book a 15-minute portfolio review with our team.]